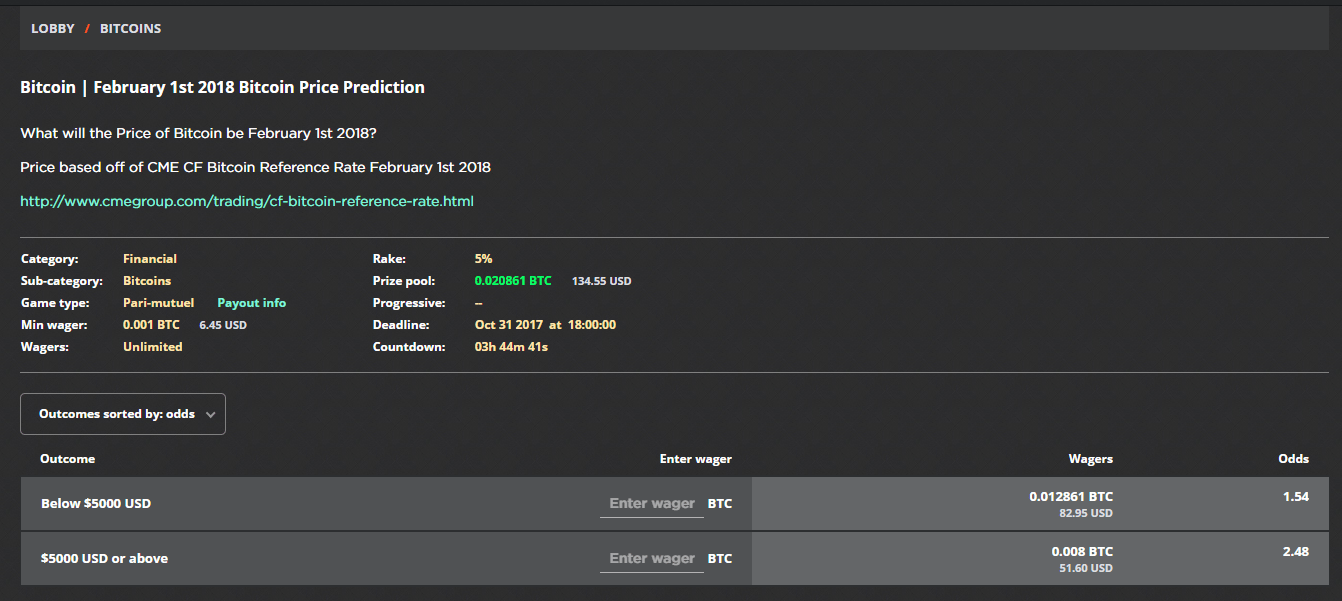

This post will describe how to use binary options to estimate the odds of a pari-mutuel pool. Friends of mine run a fantasy sports site called CoinRoster where they host pari-mutuel pools on a variety of topics including the bitcoin price. The CoinRoster bitcoin pools are fairly straight forward, users are presented with a binary question such as “will the bitcoin price be over/under a fixed price at a future date”. As the image below shows, at the time of writing, CoinRoster had a pool asking whether the price of bitcoin will be above or below $5,000 USD on February 1st 2017 based on the CME reference price. This pool closes in a few hours with the current bitcoin price is $6,352.

This is a simple market with two possible outcomes, the price will either be $5,000 and above, or below $5,000 as described by the pool’s terms. With the current price of $6,352, we can use a binary options calculator to determine the theoretical price for each outcome. We can even go a step further by converting the binary option price into an odds number format that you prefer, in the example below, I use decimal odds.

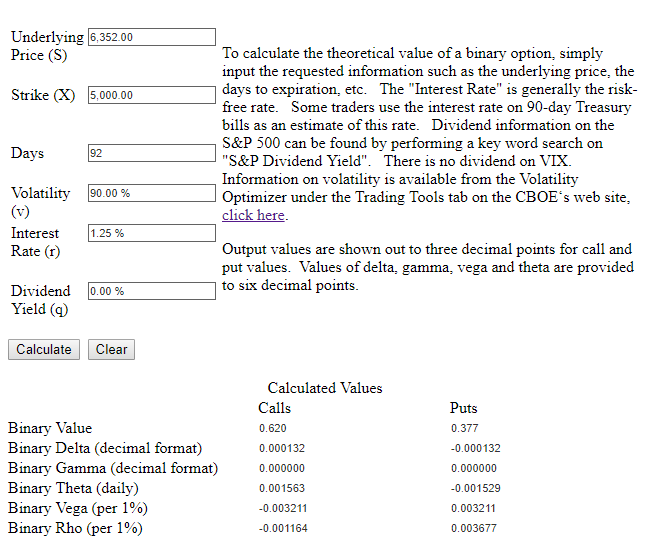

To start, let’s tally all the information we need to price the binary option:

| Days Till Expiration | 92 |

| Strike Price | $5,000 |

| Underlying Price | $6,352 |

| Volatility | 90% |

| Risk Free Rate | 1.25% |

| Distributions | 0 |

The days till expiration is the settlement date of the pool, in this case, the pool closes on October 31st, and settles based on the February 1st price, this is 92 days. The strike price is $5,000 since this is the price that the pool uses to determine the outcome (either above or below). The underlying price is the current price of bitcoin, which is $6,352. To estimate the volatility, I used the average implied volatility rate for options on deribit.com, I chose a level of 90%. I used a risk free rate of 1.25% and there are no dividends or distributions which might impact the price, so this number is zero.

Now we have all the variables, to determine the binary option prices, simply visit a free binary options calculator online and plug in the numbers, below is a screenshot.

With these variables entered, we get a result of a binary call price of 0.62 and a put price of 0.38. The first thing we should notice is since there are only two possible outcomes, the sum of call and put prices should be exactly 1.00. We should also notice that the call option is worth much more than the put option, this makes intuitive sense since the strike price is $5,000, while the underlying price is currently $6,352, making the call option “in the money”.

The binary option values can also be viewed as percentage chances, in other words, a binary option value of 0.62 is like saying there is a 62% chance of the outcome happening. To convert the binary option into an odds format such as decimal odds, simply divide 1 into the binary price = 1 / 0.62 = 1.612 or oppositely 1 / 0.38 = 2.63. Now we have an estimated price for each outcome in this pool, 1.612 for above and 2.63 for below.

In this example, the main variable that will impact the calculation is the volatility rate. We could assume different levels of volatility and get much different results. For example, instead of using a volatility level of 90%, if we used a level of 30%, the result would be binary prices of 0.935 call and 0.065 put. This makes intuitive sense since the less volatile the underlying is, the less likely it is to make big swings “out of the money” in this case, below $5,000 by February 1st.

The CoinRoster bitcoin pools are fun ways to bet on the price of bitcoin, whether you are hedging or speculating.